You file a

tax return showing tax due (before withholdings) of $503.

You have

withholdings of $1,214.

You

therefore have a refund of $711 ($1,214 - $711).

The IRS

takes your refund because you owe taxes for another year.

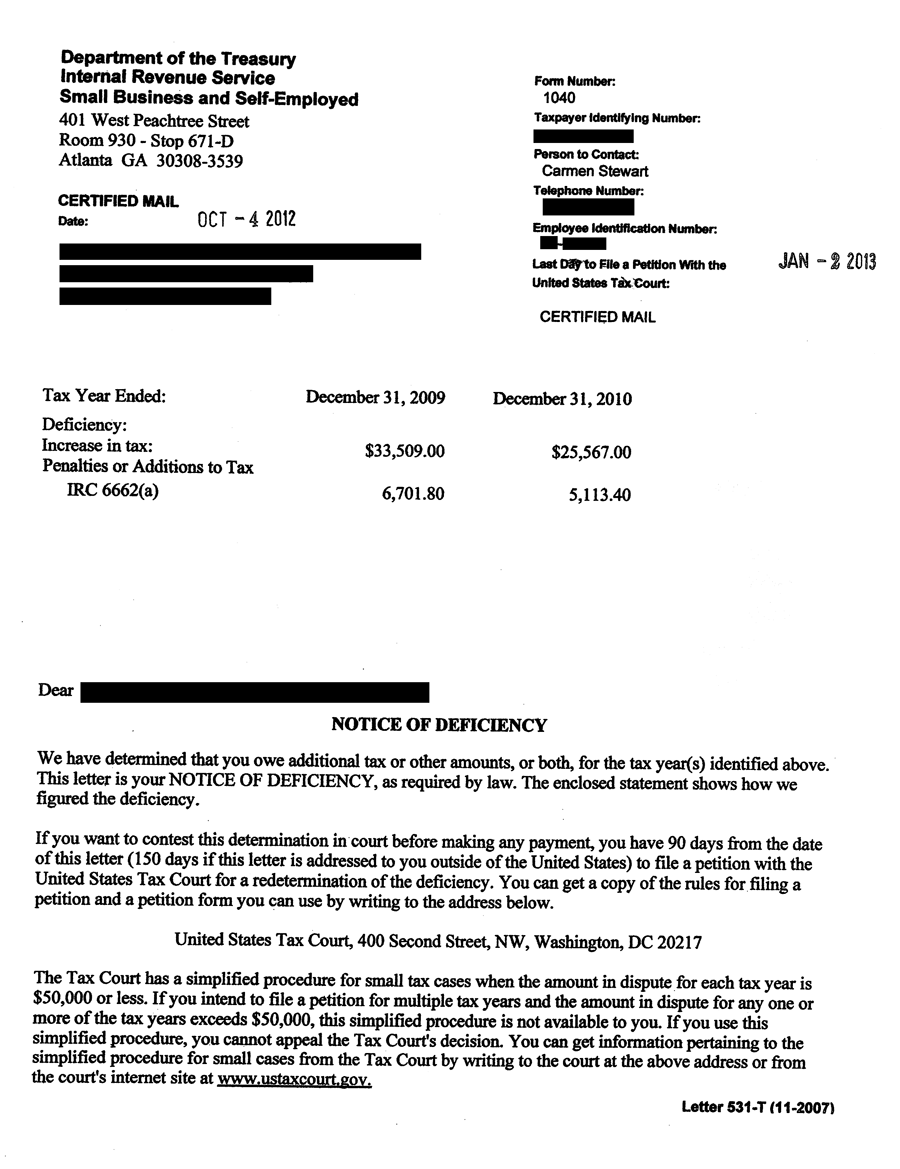

The IRS later

audits your return. It turns out that you owe another $1,403.

Question: Can you get back the $711 that went

who-knows-where?

The tax lingo

is the “right of offset.”

Here is Code section 6402(a):

(a) General rule

In the

case of any overpayment, the Secretary, within the applicable period of

limitations, may credit the amount of such overpayment, including any interest

allowed thereon, against any liability in respect of an internal revenue tax on

the part of the person who made the overpayment and shall, subject to … refund

any balance to such person.

The pace car

in this area was Pacific Gas &

Electric Co v U.S.

Pacific Gas &

Electric had an overpayment for 1982 of almost $37 million. It filed for a refund,

and the IRS included interest for sitting on PG&E’s money well into 1988. However,

the IRS miscalculated and overpaid interest by approximately $3.3 million.

The IRS

wanted its money back, but what to do?

In 1992 PG&E

filed another refund on the same tax year!

So the IRS lopped-off

$3.3 million as an “offset” for the earlier interest overpayment.

On to Court

they went. There were tax-nerd issues, such as the tax years under dispute having

closed under the statute of limitations. That issue did not concern the Court.

What did concern the Court was whether the IRS was correct in shorting a tax refund

by its previous overpayment of interest.

The IRS can clearly

offset for a tax.

But was the interest

paid PG&E the equivalent of a tax?

And the

Court decided it was not:

· Interest you (as a taxpayer) owe the

IRS is considered a “deemed” tax thanks to Section 6601(e).

Any reference to this

title (except subchapter B of chapter 63, relating to deficiency procedures) to

any tax imposed by this title shall be deemed also to refer to interest imposed

by this section on such tax.”

· But there is no Code section going the

other way - that is, when the IRS pays you interest.

PG&E won

its case and kept the interest.

Back to our

taxpayer.

He did not

have a chance of having the IRS return the $711 it had previously applied to

another tax year. What made his case interesting is that his offset year was

audited, resulting in an addition to his tax. It made sense that he would want his

withholding to be applied to its proper tax year before the IRS went offsetting

everything in sight.

It made

sense but it was not the correct answer. The IRS’ authority to offset is quite broad.

BTW, the

offset is not just for taxes. It can be for student loans or monies owed to

state agencies (think child support). The

offset is not limited to your tax refund either: your federal retirement and

social security can also be offset.