Let’s talk about

an IRS trap.

It has to do

with procedure.

Let’s say

that the you start receiving notices from the IRS. You ignore them, perhaps you

are frightened, confused or unable to pay.

Granted, I

would point out that this is a poor response to the chain-letter sequence you

will be receiving, but it is a human response. It happens more frequently than

you might think. Too many times I have been brought into these situations

rather late, and sometimes options are severely limited.

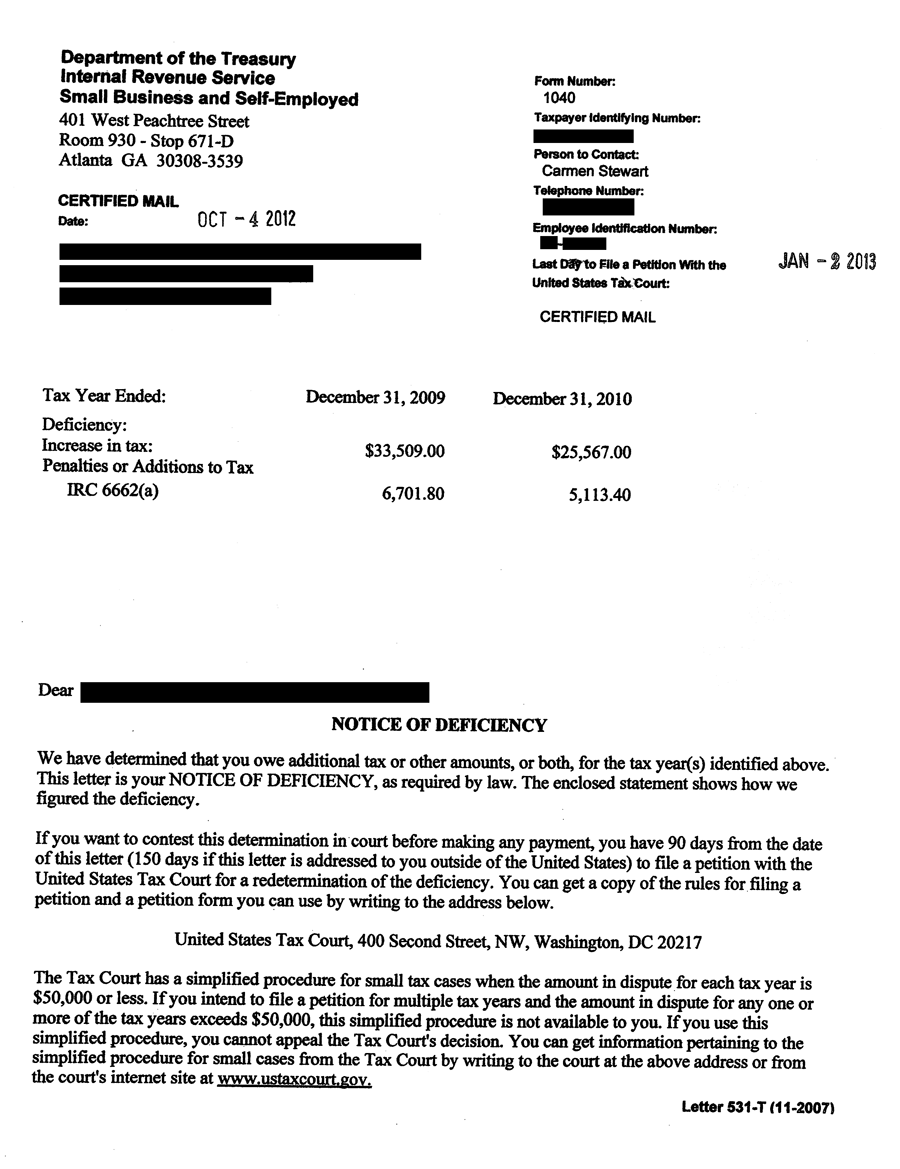

The BIG

notice from the IRS is called a 90-day letter, also known as a Statutory Notice

of Deficiency. Tax nerds refer to it as a SNOD.

This is the

final notice in the chain-letter sequence, so one would have been receiving correspondence

for a while. The IRS is going to assess, and one has 90 days to file with the

Tax Court.

Assessment

means that the IRS has 10 years to collect from you. They can file a lien, for

example, and damage your credit. They might levy or garnish, neither of which

is a good place to be.

I have

sometimes used a SNOD as a backdoor way to get to IRS appeals. Perhaps the

taxpayer had ignored matters until it reached critical mass, or perhaps the

first Appeals had been missed or botched. I had a first Appeals a few years

back with a novice officer, and her lack of experience was the third party on our

phone call.

Let the 90

days run out and the Tax Court cannot hear the case.

NOTE: Most times a Tax Court filing never goes to court. The Tax Court does not want to hear your case, and the first thing they do is send it back to Appeals. The Court wants to machinery to solve the issue without them getting involved.

Our case

this time involves Caleb Tang. He filed pro se with the Tax Court, meaning that

he represented himself. Technically Caleb does not have to go by himself – he can

hire someone like me – but there are limitations.

There is a

game here, and the IRS has used the play before.

The taxpayer

makes a mistake with the filing. In our story, Caleb filed but he forgot to pay

the filing fee.

Technically

this means the Court would not have jurisdiction.

Caleb also

filed an amended return.

As I said,

sometimes there are few good options.

The IRS

contacted Caleb and said that they would not process his amended return unless

he dropped the Tax Court petition.

Trap.

You see, Caleb

was past the 90-day window. If he dropped his filing, the IRS would automatically

get its assessment, and Caleb would have no assurance they would process his

amended return.

Caleb would then

not be able to get back to Tax Court. Procedure requires that he pay the tax

and then sue in District Court or Court of Federal Claims. There is no pro se in

that venue, and Caleb would have no choice but to hire an attorney.

That will

weed out a lot of people.

Fortunately,

the Court (Chief Judge L Paige Marvel) knew this.

He allowed

Caleb additional time to pay his application fee.

Meaning that

the case got into the Tax Court’s pipeline.

What happens

next?

It could go

three different ways:

(1) Both parties drop the case.

(2) They do not drop the case and the matter

goes back to Appeals.

(3) The Court hears the case.

I suspect

the IRS will process Caleb’s amended return now.