I had a moment of dual disbelief and laughter.

At the expense of the IRS and the Tax Court.

Electronic records, cloud computing and work from home

(WFH) have and continue to revolutionize the way we practice and work. I have

been working, for example, with a CPA firm sponsoring a very robust WFH policy, as

well as outsourcing selected tax functions overseas. Mind you, the infrastructure

protecting that data transmission and retention is formidable, but woe to the accountant

- especially if over age 40 – learning it for the first time.

Let’s go back to 2020. The Tax Court was rolling-in

its new electronic platform – called DAWSON - which in turn was based on PACER,

used for dockets in other courts. The Court was embracing electronic records,

albeit in fits and starts. For example, the initial launch included only

records created by the Court itself. It did not include taxpayer-submitted

documents, for example. While the intent to protect taxpayer privacy was clear,

it was also clear that some compromise was required. Filings containing confidential

information could be sealed. If not otherwise pertinent, any confidential information

could be redacted in the filing copy.

DAWSON did allow for electronic filing of the court petition itself.

This was a big deal.

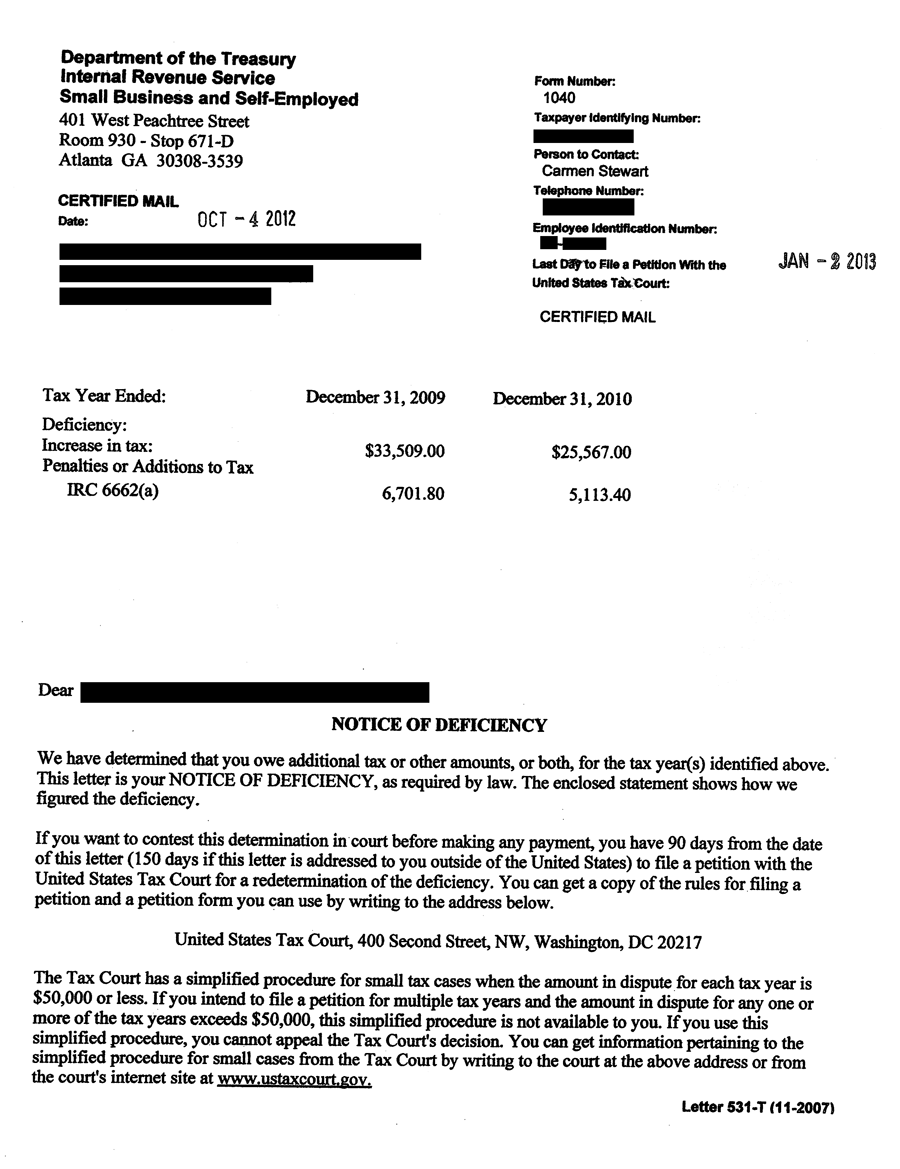

We have spoken many times about a Notice of Deficiency

(NOD) or Statutory Notice of Deficiency (SNOD). This is an IRS notice, and it

is also known as the 90-Day Letter. That 90 days may well be cast in concrete,

as you have 90 days to file with the Tax Court should you choose to contest the

matter. The IRS is very unforgiving here: miss the deadline by one day and it

is guaranteed that the IRS will move to toss out your petition.

The electronic filing provides some piece of mind, but

accidents still happen.

EXAMPLE: Antawn Jaal Sanders was filing electronically with the Tax Court, but Antawn cut it close. The last day to file was December 12, 2022, and Antawn had started downloading the Court forms onto his Android shortly before 10 p.m. Unable to file from his phone, he switched to his computer at 11:56 p.m. It took him a minute to log in and several to return to where he had been. It was after midnight by the time he started uploading to DAWSON. The IRS of course moved to dismiss his petition, and the Court agreed. Antawn might challenge the IRS, but he was not doing it in Tax Court. After midnight was the next day, meaning his petition was late.

Do you wonder how the taxpayer signs that petition in

DAWSON?

If it were a paper file, there would be a handwritten

signature.

DAWSON does not allow (for now, at least) for a

handwritten signature. What it does do is allow a block-letter facsimile of

your signature.

Here is the Court:

The combination of DAWSON username (email address) and password serves as the signature of the individual filing the document.”

The Court says it will accept the facsimile as a

signature, so that should be the end of it.

Except when it isn’t.

Robert and Kegan Donlan filed their petition on

DAWSON, and they took advantage of the electronic signature.

The IRS immediately filed a Motion to Dismiss, arguing

that the Court lacked jurisdiction to hear the case because the petition was

not property signed.

The Court bounced the IRS motion, of course.

And I find myself wondering – why did the IRS go

there? I suppose it simply had to test the lock, fully expecting it to be

locked.

And – here is years of CPA practice speaking – whether

it was a new attorney who drew the short straw to look foolish in front of the

Court.

Our case this time was Donlan v Commissioner,

U.S. Tax Court Docket 16579-24, Feb. 19, 2025.