I am looking at a case involving the premium tax

credit.

We are talking about the Affordable Care Act, also

known as Obamacare.

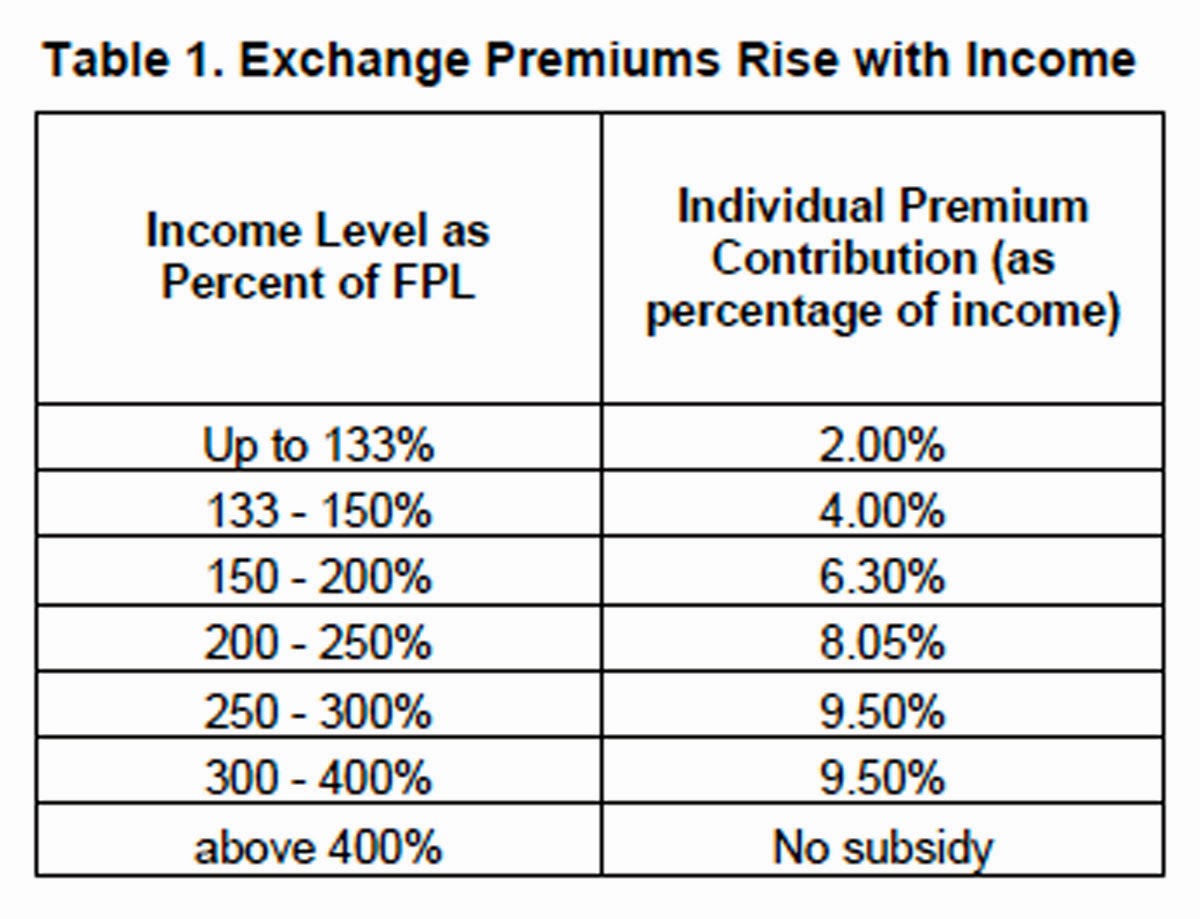

Obamacare uses mathematical tripwires in its

definitions. That is not surprising, as one must define “affordable,” determine

a “subsidy,” and - for our discussion – calculate a subsidy phase-out. Affordable

is defined as cost remaining below a certain percentage of household income.

Think of someone with extremely high income - Elon Musk, for example. I

anticipate that just about everything is affordable to him.

COMMENT: Technically the subsidy is referred to as the “advance premium tax credit.” For brevity, we will call it the subsidy.

There is a particular calculation, however, that is brutal.

It is referred to as the “cliff,” and you do not want to be anywhere near it.

One approaches the cliff by receiving the subsidy. Let’s say that your premium would be $1,400 monthly but based on expected income you qualify for a subsidy of $1,000. Based on those numbers your out-of-pocket cost would be $400 a month.

Notice that I used the word “expected.” When

determining your 2022 subsidy, for example, you would use your 2022 income.

That creates a problem, as you will not know your 2022 income until 2023, when

you file your tax return. A rational alternative would be to use the prior

year’s (that is, 2021’s) income, but that was a bridge too far for Congress.

Instead, you are to estimate your 2022 income. What if you estimate too high or

too low? There would be an accounting (that is, a “true up”) when you file your

2022 tax return.

I get it. If you guessed too high, you should have

been entitled to a larger subsidy. That true-up would go on your return and

increase your refund. Good times.

What if it went the other way, however? You guessed

too low and should have received a smaller subsidy. Again, the true-up would go

on your tax return. It would reduce your refund. You might even owe. Bad times.

Let’s introduce another concept.

ACA posited that health insurance was affordable if

one made enough money. While a priori truth, that generalization was unworkable.

“Enough money” was defined as 400% of the poverty level.

Below 400% one could receive a subsidy (of some amount).

Above 400% one would receive no subsidy.

Let’s recap:

(1) One could receive a subsidy if one’s income

was below 400% of the poverty level.

(2) One guessed one’s income when the subsidy

amount was initially determined.

(3) One would true-up the subsidy when filing

one’s tax return.

Let’s set the trap:

(1) You estimated your income too low and received

a subsidy.

(2) Your actual income was above 400% of the

poverty level.

(3) You therefore were not entitled to any subsidy.

Trap: you must repay the excess subsidy.

That 400% - as you can guess – is the cliff we

mentioned earlier.

Let’s look at the Powell case.

Robert Powell and Svetlana Iakovenko (the Powells)

received a subsidy for 2017.

They also claimed a long-term capital loss deduction

of $123,822.

Taking that big loss into account, they thought they were

entitled to an additional subsidy of $636.

Problem.

Capital losses do not work that way. Capital losses

are allowed to offset capital losses dollar-for-dollar. Once that happens,

capital losses can only offset another $3,000 of other income.

COMMENT: That $3,000 limit has been in the tax Code since before I started college. Considering that I am close to 40 years of practice, that number is laughably obsolete.

The IRS caught the error and sent the Powells a

notice.

The IRS notice increased their income to over 400% and

resulted in a subsidy overpayment of $17,652. The IRS wanted to know how the

Powells preferred to repay that amount.

The Powells – understandably stunned – played one of

the best gambits I have ever read. Let’s read the instructions to the tax form:

We then turn to the text

of Schedule D, line 21, for the 2017 tax year, which states as follows:

If line

16 is a loss, enter ... the smaller of:

· The

loss on line 16 or

· $3,000

So?

The Powells pointed out that a loss of $123,822 is

(technically) smaller than a loss of $3,000. Following the literal instructions,

they were entitled to the $123,822 loss.

It is an incorrect reading, of course, and the Powells

did not have a chance of winning. Still, the thinking is so outside-the-box

that I give them kudos.

Yep, the Powells went over the cliff. It hurt.

Note that the Powell’s year was 2017.

Let’s go forward.

The American Rescue Plan eliminated any subsidy

repayment for 2020.

COVID year. I understand.

The subsidy was reinstated for 2021 and 2022, but

there was a twist. The cliff was replaced with a gradual slope; that is, the

subsidy would decline as income increased. Yes, you would have to repay, but it

would not be that in-your-face 100% repayment because you hit the cliff.

Makes sense.

What about 2023?

Let’s go to new tax law. The ironically named

Inflation Reduction Act extended the slope-versus-cliff relief through 2025.

OK.

Congress of course just kicked the can down the road,

as the cliff will return in 2026.

Our case this time was Robert Lester Powell and

Svetlana Alekseevna Iakovenko v Commissioner, T.C. Summary Opinion 2002-19.