It is called

the “premium assistance tax credit,” and it refers to the subsidy that people

will receive under the ObamaCare individual mandate. It will begin in 2014, and

it is supposed to make insurance more affordable for people under 400% of the

federal poverty line (FPL). I am not really sure how the politicians came up

with 400%, as many if not most of us would agree that 4 times the poverty line

is nowhere near poverty. For example, if you are married and have a child, 400%

of the FPL is $78,120. That picks up a lot, if not the majority, of people in the

Cincinnati area.

OBSERVATION: I did not realize that Washington views the average

Cincinnatian as impoverished and in need of their help. How did we ever survive this blight before?

Starting

next year, you have to address your health insurance, either by receiving it

through work, remaining on your parent’s policy, buying it in the private

marketplace or on the public exchange. If you don’t, tax advisors are supposed

to calculate a tax penalty when preparing your 2014 taxes in April 2015. If you

do, then tax advisors may have to go through a separate calculation to

determine whether the government paid too much or too little subsidy toward your

health insurance. As a tax advisor, I say … whoopee. You would think the

government could at least put me on its 401(k) plan for doing its yeoman work.

So how do you calculate whether the government

paid too much or too little? That is our topic this week.

We will need

two tables to do this. The first is the FPL table by household size.

The second

table provides the phase-out of the subsidy as one’s income increases through

the FPL table.

When you and

I meet in April 2015, I will know your 2014 adjusted gross income (AGI), which

starts off this exercise. A good definition of AGI is the amount of money you

made before you deduct your house, taxes, contributions and kids. I will then have

to make some adjustments to it, if you have certain items on your return:

·

I

will add tax -exempt interest

·

I

will add the untaxed portion of your social security

·

If

you worked overseas I will add the exempted portion of your salary

You now have

something called modified adjusted

gross income (MAGI).

Let’s say

that you are married, have a toddler and your MAGI is $55,000. You have a

modest home, an older car and are living the dream.

The table

tells me that you are under 400% of the FPL (which is $78,120 for a family of 3),

so we next talk about your health insurance. You tell me that you do not have

insurance at work. Your wife is staying at home and being a mom. You went and

bought a health policy on the public exchange. You purchased an Anthem bronze

plan costing $715 per month. That $715 however was before the subsidy, to which

we will return in a moment.

We now have

your actual 2014 income, and we have to settle-up with the government. If you

were under-subsidized, you will get a check. If you were over-subsidized, you

have to return the money.

NOTE: The subsidy is being paid directly to the insurer. You

never see this check. It is very possible that you never even paid attention to

the subsidy amount, as you were focusing only on your out-of-pocket.

At MAGI of $55,000,

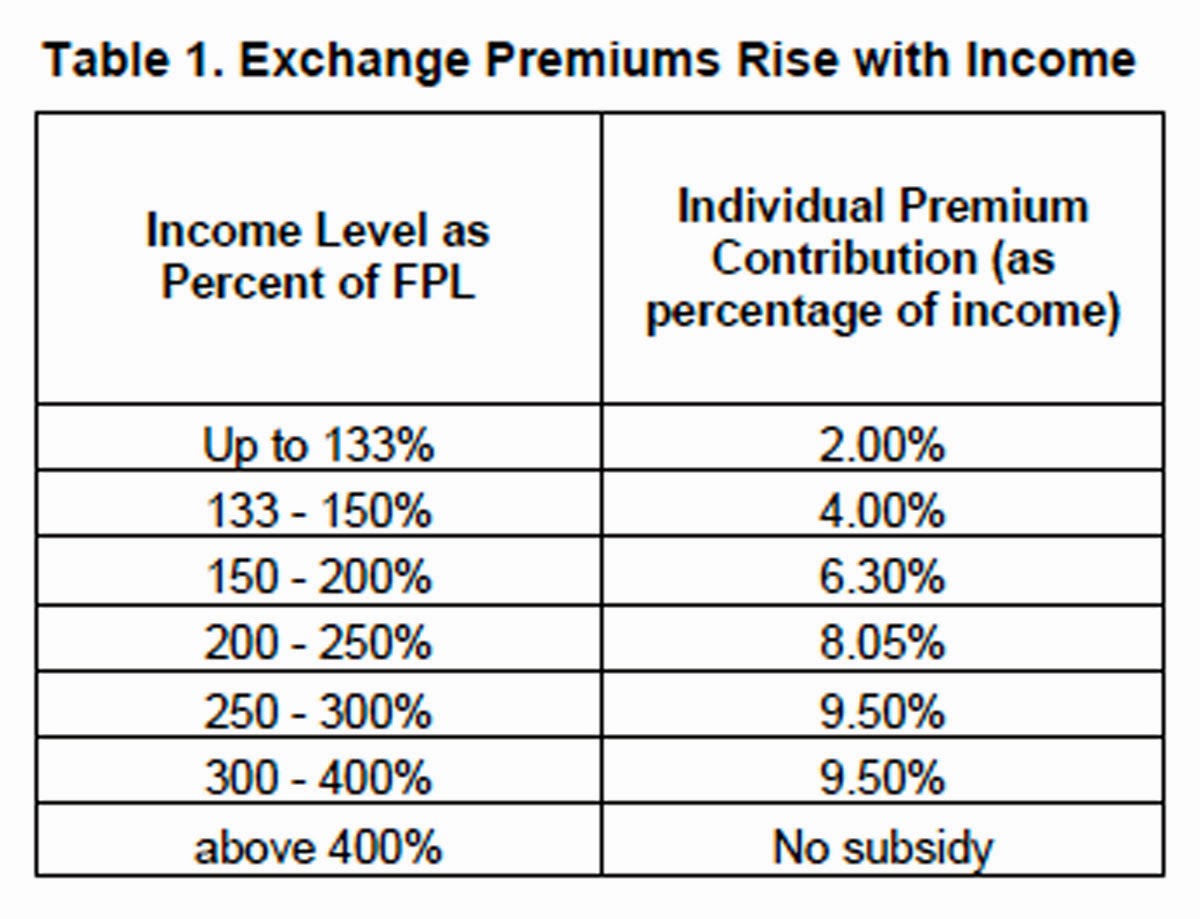

you are at 282% of the FPL ($55,000/$19,530). We now go to the next table. There

is a sliding scale between 250% and 300% FPL, going from 8.05% to 9.5% of MAGI.

You are somewhere in the middle, so we have to do some math:

282 – 250 = 32

32/50 = 64%

9.5% - 8.05% = 1.45%

1.45% * 64% = 0.93%

8.05% + 0.93% = 8.98%

Your

premiums are limited to 8.98% of your MAGI. As we said, your income was $55,000.

That means your share of the premiums caps-out at $4,939.

How much was

your subsidy? Total annual premiums were $8,580 ($715 * 12 months). Your cap is

$4,939. The difference is $3,641, or $303 per month. If your subsidy was less

than $303/month, I have good news for you. If it was more, then I have bad news,

as you will be writing the government a check.

How do we know the subsidy? There will be a new tax form – Form 1095-A-

that will be issued about the same time as your W-2. You will have to bring

that form to me when preparing your taxes.

There are

limits on how much you have to repay the government:

·

If

you are below 200% of the FPL, the most you have to pay back is $600

·

Between

200% and 300% the maximum is $1,500

·

Between

300% and 400% the maximum is $2,500

The

$600/$1,500/$2,500 limits are for a family. It is one-half that amount if you

are single.

By the way

…. IF your MAGI exceeds 400% FPL, then you have to repay ALL the subsidy with

your tax return.

The above

limits ($600/$1,500/$2,500) do not apply if the government owes you. This could

happen if your income dropped significantly, such as your employer moving you

to part-time.

You may have

read that the White House delayed the employer reporting for one year. It will

now start in 2015 (for 2014), rather than 2014 (for 2013). The White House believes

that it has limited the potential for fraud because of the requirement to

settle-up the individual mandate when filing the individual income tax return. You

can see their point.

I am very

uncomfortable with this action, however. Since when does a White House get to

decide which laws it wants to enforce and which laws it does not? What if the

next president decides to “suspend” the corporate tax for a year? This White

House is creating precedence for that White House to do so.

What we have

now are three categories of health consumers:

(1) Over 400%: you pay full boat. The

exchanges and subsidies mean nothing to you.

(2) Between 133% and 400% of the FPL: you

may be subject to the above, depending upon your insurance situation at work.

(3) Below 133%: you are likely enrolled

in Medicaid and pay no premiums at all. This however will vary by state, as

many states did not participate in the Medicaid expansion under ObamaCare.

You cannot

deduct the portion of your health insurance that is being subsidized. However,

since the medical deduction threshold is increasing to 10% (from 7.5%) of AGI,

it is highly unlikely that you will ever deduct medical expenses again, unless

you have exceptional circumstances.

And there is

how the government intends that people will settle up their ObamaCare if they

qualify for a subsidy. Seems reasonable, as in

I-haven’t-been-in-the-real-world-and-earned-a-real-paycheck-for-many-years-now and how-hard-can-it-be-to-build-a-website sort

of way.

After all,

what could possibly go wrong?

No comments:

Post a Comment