It is one of my least favorite areas of individual tax

practice.

We are talking about health insurance. More

specifically, health insurance purchased through the exchanges, coupled with

advance payment of the premiums.

Why?

Because there is a nasty tax trap in there, and I saw the

trap again the other day. It caught a client who gets by, but who is hardly in

a position to service heavy tax debt.

Let’s set it up.

You can purchase health insurance in the private

market or from government-sponsored marketplaces – also called exchanges. The exchanges

were created under the Affordable Care Act, more colloquially known as

Obamacare.

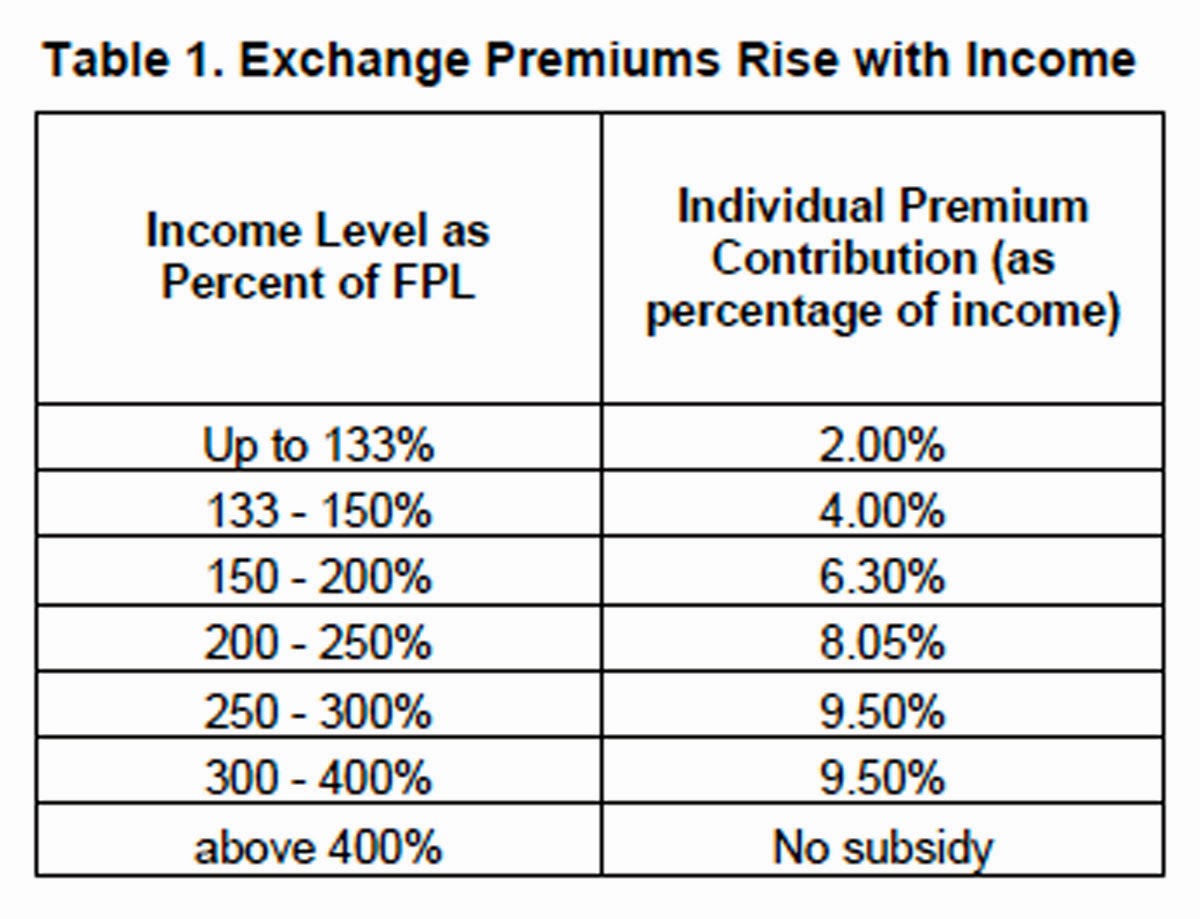

If you purchase health insurance through the exchange and

your income is below a certain level, you can receive government assistance in

paying the insurance premiums. Make very little income, for example, and it is

possible that the insurance will be free to you. Make a little more and you

will be expected to contribute to your own upkeep. Make too much and you are

eliminated from the discussion altogether.

The trap has to do with the dividing line of “too

much.”

Let’s look at the Abrego case.

Mr and Mrs Abrego lived in California. For 2015 he was

a driver for disabled individuals, and he also prepared a few tax returns

(between 20 and 30) every year. Mrs Abrego was a housekeeper.

They enrolled in the California exchange. They also

did the following:

(1) They provided an estimate of their income for

2015. Remember, the final subsidy is ultimately based on their 2015 income,

which will not be known until 2016. While it is possible that someone would

purchase health insurance, pay for it out-of-pocket and eventually get

reimbursed by the IRS when filing their 2015 tax return in 2016, it is far more

likely that someone will estimate their 2015 income to then estimate their

subsidy. One would use the estimated subsidy to offset the very real monthly

premiums. Makes sense, as long as all those estimated numbers come in as

expected.

(2) They picked a policy. The monthly premiums

were $1,029.

(3) The exchange cranked their expected 2015

numbers and determined that they could personally pay $108 per month.

(4) The difference - $ 1,029 minus $108 = $921–

was their monthly subsidy.

The Abregos kept this up for 10 months. Their total 2015 subsidy was $9,210 ($921

times 12).

Since the Abregos received a subsidy, they had to file

a tax return. One reason is to compare actual numbers to the estimated numbers.

If they guessed low on income, they would have to pay back some of the subsidy.

If they guessed high, the government would owe them for underestimating the

subsidy.

The Abregos filed their 2015 return.

They reported $63,332 of household income.

How much subsidy should they have received?

There is the rub.

The subsidy changes as income climbs. The subsidy gets

to zero when one hits 400% of the poverty line.

What was the poverty line in California for 2015?

$15,730 for a married couple.

Four times the poverty line was $62,920.

They reported $63,332.

Which is more than $62,920.

By $412.

They have to pay back the subsidy.

How much do they have to pay back?

All of it - $9,210.

Folks, the tax rate on that last $412 is astronomical.

It is frustrating to see this fact pattern play out. The

odds of a heads-up from the client while someone can still do something are –

by the way – zero. That leaves retroactive tax planning, whose success rate is also

pretty close to zero.

Our client left no room to maneuver. Why did her

income go up? Because she sold something. Why did she not call CTG galactic command

before selling – you know: just in case? What would we have done?

Probably advised her to NOT SELL in the same year she is receiving a government

subsidy.

How did it turn out for the Abregos?

They should have been toast, except for one thing.

Remember that he prepared tax returns. He did that on

the side, meaning that he had a gig going. He was self-employed.

He got to claim business deductions.

And he had forgotten one.

How much was it?

$662.

It got their income below the magic $69,920 level.

They were on the sliding scale to pay back some of

that subsidy. Some - not all.

It was a rare victory in this area.

Our case for the homegamers was Abrego v

Commissioner.