Let’s go

hard procedural on this post.

He played

defensive end in the NFL with the Tennessee Titans and Philadelphia Eagles from

1999 to 2010. At 6’4”, 260 pounds, 86-inch wingspan and 4.43 forty, NFL fans

remember him as “The Freak.”

Jevon Kearse

is in the tax literature.

It looks

like a business deal went bad, because in 2010 he claimed a $1,359,000 bad debt

deduction.

The IRS

bounced it. The IRS

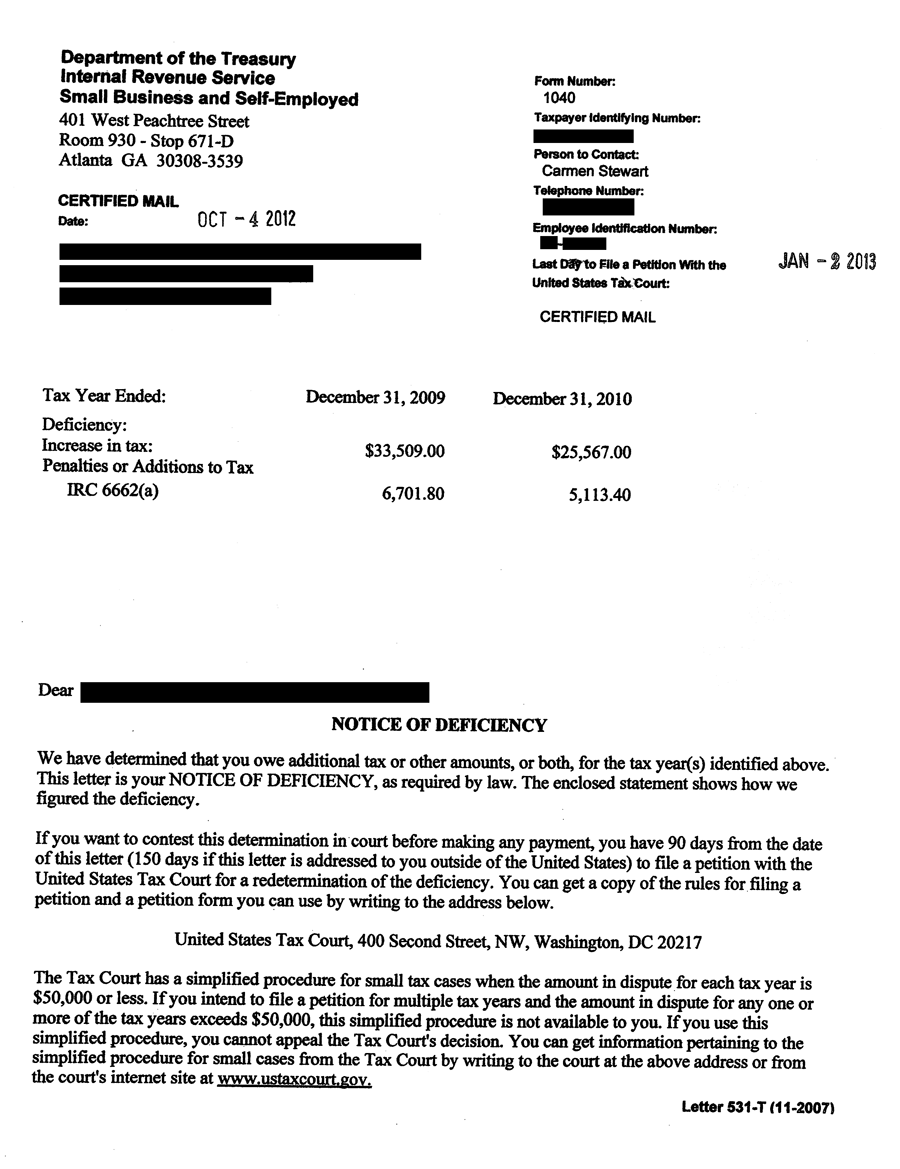

now wanted over $430 thousand in tax. They issued a Notice of Deficiency (NOD) on

May 11, 2012.

COMMENT: Procedurally, the IRS issues a NOD (also known as a SNOD) before it can officially assess the additional tax. Once assessed, the IRS can bring all its collection powers to bear.

Problem:

Kearse says he never received the NOD.

Let us start

our walk through IRS procedure.

Once

assessed, the IRS sent Kearse a Notice of Federal Tax Lien.

COMMENT: One has the right to request a hearing (called a Collection Due Process hearing) in response.

Kearse

requested a CDP hearing, at which he asserted that he never received the NOD

and presented an offer in compromise (liability – for the home gamers) for $1.

COMMENT: There are three flavors of offer in compromise. The one we are talking about is when there is substantial doubt that the assessed tax is correct. At $1, that is exactly the point Kearse was making.

IRS Appeals tuned him down, and off to Tax

Court they went.

A taxpayer

has the right to challenge the underlying tax liability in a CDP hearing IF he/she never received the NOD or

otherwise never had a chance to dispute the proposed assessment. This is a procedural

requirement, and the Court can bring it up even if the taxpayer fails to.

Responsibility

now shifted to the IRS. The Appeals officer had to prove that the IRS properly

mailed the NOD. There are two general ways to do this:

(1) Reviewing an internal IRS document

management system

(2) Reviewing a postal Form 3877 or an equivalent

mailing list with date stamps and/or initials.

The IRS said

they did the first option: they reviewed the internal system.

Kearse’s tax

attorneys also got the Appeals officer to stipulate that she could not produce

a Form 3877 or otherwise prove the mailing of the NOD.

NOTE: We will come back to the importance of a “stipulation” in a moment.

There is a

second procedural issue here: the IRS can rely on its internal system unless

the taxpayer alleges that the NOD was not properly mailed.

Which is

what Jevon Kearse had done. The IRS could not rely on option (1).

Incredibly,

the IRS finally found the Form 3877, explaining that the eventual success had

resulted from an update to their systems.

The Court

bounced the Form 3877.

What ….?

It has to do

with the stipulation. You see, a stipulated fact is treated as conclusive

evidence. It cannot be changed, barring extraordinary circumstances.

The IRS had

to argue extraordinary circumstances.

And we have

the third procedural issue: the IRS failed to do so.

Meaning the

IRS was bound by its stipulation that it could not prove the mailing of the

NOD.

The IRS

attorney flubbed.

Jevon Kearse

won.

What a freak

case.