I am reading a case about cancellation of indebtedness income.

Let’s take a moment to discuss the concept of income in the tax Code.

The 16th amendment, passed in 1913 and authorizing a federal income tax, reads as follows:

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

Needless to say, the definition of “incomes, from whatever source” became immediately contentious.

Ask a tax practitioner for a definition of income, and it is likely that he/she will respond with “an accession to wealth.”

That phrase comes from a 1955 Supreme Court case (Commissioner v Glenshaw Glass) which included the following:

Here, we have instances of undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion."

I am seeing three conditions, of which “accession to wealth” is but one.

Let’s circle back

to indebtedness and income.

Can one have income by borrowing money?

Unless there is something extraordinarily odd about the loan, I would say “no.” The reason is that any increase in wealth (by receipt of the loan proceeds) is immediately offset by the requirement to repay the loan.

Let’s say you buy a house. You take out a mortgage.

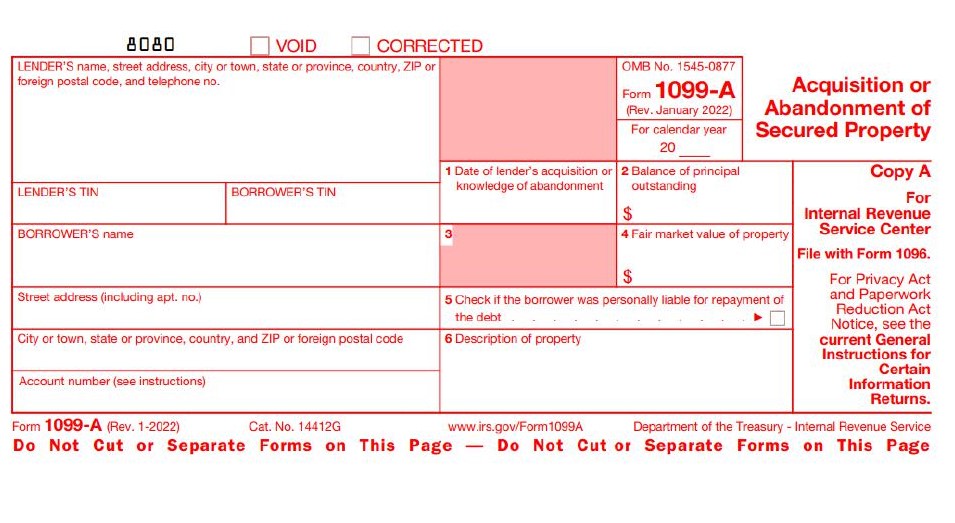

What if you are in financial distress and mail the keys back to the mortgage company?

Granted, the house secures the debt, but surrendering the house does not automatically release the debt. It however will likely result in your receiving the following 1099:

Like any 1099, there is a presumption of income. In this instance, there has been an exchange in the ownership of the house. There is another way to say this: the tax Code sees a sale of the property.

It seems odd that tax sees potential income here. It is unlikely to happen if the surrendered asset is one’s principal residence, as one would have access to the $250,000/$500,000 gain exclusion. It could happen if the surrendered asset is rental or investment property, though.

What about the debt on the property?

Tax considers that a separate transaction.

When the debt is discharged, the IRS has yet another form:

Yes, it gets confusing. The system works much better when the two steps happen concurrently – such as in a short sale. In that case, it is common to skip the 1099-A altogether and just issue the 1099-C.

NOTE: There is a twist in the straw depending upon whether the debt is recourse or nonrecourse. Believe it or not, there are about a dozen states where you can buy your principal residence with nonrecourse debt. You will not be surprised to learn that California is one of them. The upside is that you can return the keys to the bank and no longer be responsible for the mortgage. The downside is this policy was a major contributor to the burst of the housing bubble in the late aughts.

It is common for the 1099-C to be issued three years after the 1099-A. Why? The Code requires the reporting of cancellation of indebtedness on or before an “identifiable event” happens.

An identifiable event in turn is defined as:

- bankruptcy

- expiration of statute of limitations for collection

- cancellation of debt that renders it unenforceable in a receivership, foreclosure, or similar proceeding

- creditor's election of foreclosure remedies that statutorily bars recovery

- cancelation of debt due to probate proceedings

- creditor's discharge pursuant to an agreement

- discharge of indebtedness pursuant to a decision by the creditor, or the application of a defined policy of the creditor, to discontinue collection activity and discharge debt

- in specific cases, the expiration of a non-payment testing period [presumption of 36 months of no payment to the creditor]

The three years is number (8).

The income type we are discussing with the 1099-C is cancellation of indebtedness income. As discussed, just borrowing money does not create income. Whereas your assets may go up (you have cash from the loan or bought something with the cash), that amount is offset by the loan itself. The scales are balanced, and there is no accession to income.

However, cancel the debt.

The scale is no longer balanced.

Meaning you have potential income.

But the Code allows for exceptions. Here is Section 108:

(a) Exclusion

from gross income

(1) In general Gross income does not

include any amount which (but for this subsection) would be includible in gross

income by reason of the discharge (in whole or in part) of indebtedness of the taxpayer if—

(A) the discharge occurs in

a title 11 case,

(B) the discharge occurs

when the taxpayer is insolvent,

(C) the indebtedness

discharged is qualified farm indebtedness,

(D) in the case of a

taxpayer other than a C corporation, the indebtedness discharged is qualified real property business indebtedness,

or

(E) the indebtedness

discharged is qualified principal residence indebtedness which

is discharged—

(i) before January 1, 2026, or

(ii) subject to an arrangement that is entered into and evidenced in writing before January 1, 2026.

The common ones are (a)(1)(A) for bankruptcy and (a)(1)B) for insolvency.

Bankruptcy is self-explanatory.

Solvency is not self-explanatory. You can think of insolvency as being bankrupt but not filing for formal bankruptcy. You owe more than you own. Let’s call the difference between the two the “hole.” To the extent that that cancelled debt is less than the “hole,” there is no cancellation of indebtedness income. Once the cancelled debt equals the “hole,” the exclusion ends. At that point, your net worth is zero (-0-). Technically the next dollar is an “accession to wealth” and therefore income.

In our case this week Ilana Jivago borrowed from Citibank. She defaulted and was eventually foreclosed on in 2009. Citibank sent her a 1099-C. Jivago argued that it was nontaxable because it was qualified principal residence indebtedness per (a)(1)(E) above.

Qualified principal residence indebtedness is defined as:

Indebtedness incurred in acquiring, constructing, or substantially improving any qualified residence of the taxpayer.

The Court looked

at photographs of and admired the renovations she made in 2005 and 2006. The

Court noted that Jivago did not use an interior designer, and she did much of

the work herself.

The problem is that 2005 and 2006 were before she borrowed from Citibank.

Easy win for the IRS.

Our case this time was Jivago v Commissioner, Docket No. 5411-21.