I was

speaking with a colleague earlier this week who wants to set up a tax storefront.

That means a place that prepares taxes, probably only individual taxes and only

for a few months a year. Think H&R Block, but without a franchise involved.

I suspect he would be successful, but like any business start-up the cash drain

is difficult to pull off.

And he asked

me if tax seasons are getting “harder.” Yes, he is younger than me. I am

getting to that age.

I hesitated

on his question, as my long-standing position is that the accounting firm

determines the difficulty of the season for its employees. Some firms do a good

job, and other firms simply do not care. It is one of the reasons that the

average career of an accountant in a CPA firm is little more than that

of an NFL player.

Bet you did

not know that.

Still, there

are issues for tax practitioners that did not exist a few years ago – or even

last year.

I was

speaking this week with a good friend about whether it was safe for him to prepare

his personal tax return on TurboTax. Depending upon the year and other factors,

he prepares a draft return and I review it for him. Last year he changed jobs

and states, so I expect I will review his return this year.

Why TurboTax?

It turns out that a number of states experienced suspicious electronic filing

activity this year and, upon investigation, in many cases the electronic return

was filed using TurboTax.

Let’s be

fair, though. That does not mean that the information came from TurboTax. There

have enough recent breeches of data security that the information may have come

from elsewhere.

Intuit, the

parent of TurboTax, responded aggressively to this development, as you would

imagine. A number of states, including Kentucky and Minnesota, temporarily halted

the processing of electronically filed returns. Meanwhile TurboTax encouraged its customers to

log-in and review their accounts. They instructed their customers to review

their direct-deposit information specifically.

Makes sense.

Why the

states? In the past, fraudsters have targeted the IRS rather heavily. The IRS responded

with stricter identity measures, including lockdowns on any tax refunds and the

required use of security passwords. Florida was so hard-hit, for example, that

one can request a federal security PIN number under a pilot program – even if

one was not the victim of identity theft.

It may be

that the fraudsters saw easier picking elsewhere.

Then we have

the information documents to prepare a tax return.

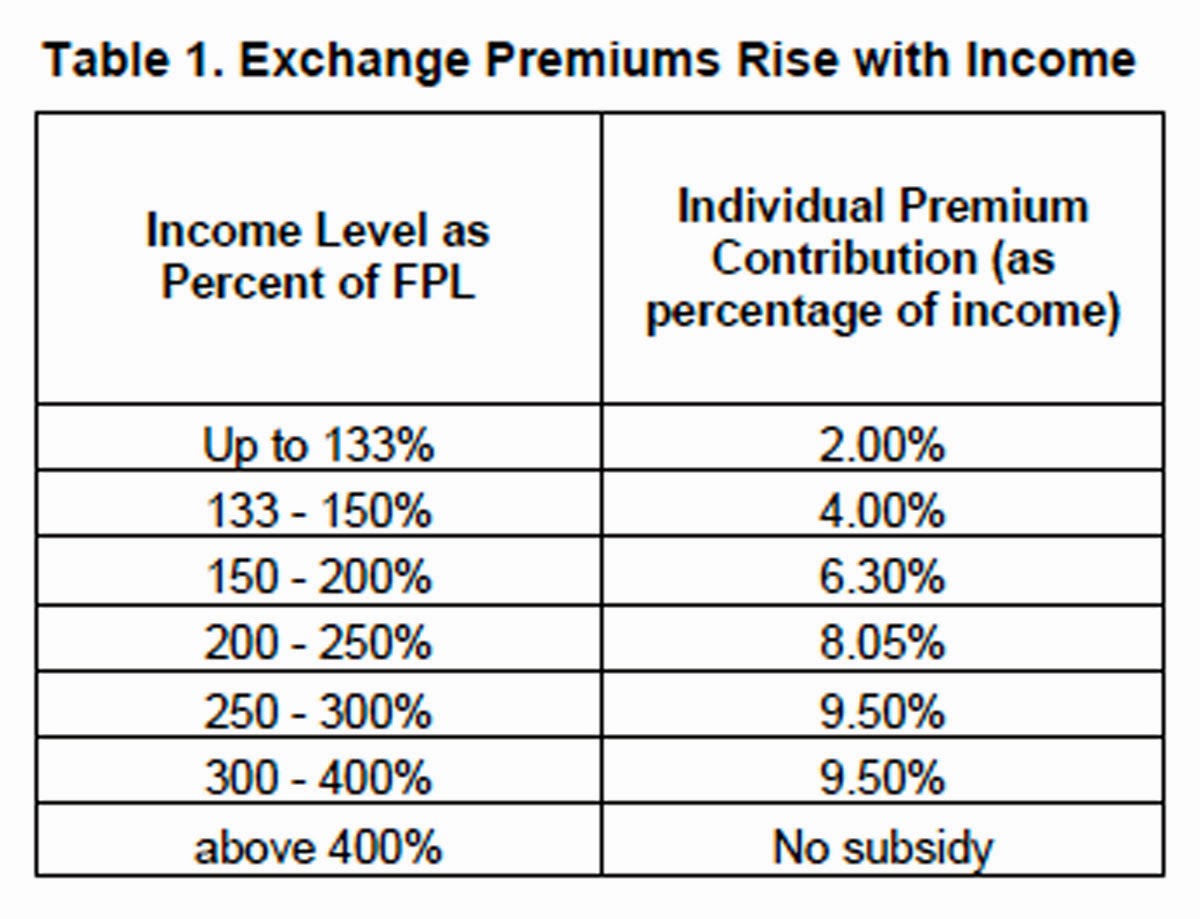

I am reading

that the federal health insurance marketplace has sent out approximately

800,000 erroneous Forms 1095-A. This is not insignificant and represents approximately

one-in-five people using the marketplace. These forms are new and are issued by

the exchanges to individuals who purchased insurance there. They include

information on any government subsidy, so they are an important tax document. For example, even if you are not otherwise

required to file a tax return, you must file if you received a subsidy.

The error

concerns the “benchmark plan” premium and doesn’t concern the amount of subsidy

itself. The “benchmark plan”” is the second lowest cost silver plan for where one

lives, and it is part of the arithmetic to settle-up whether one received too

much or too little subsidy. As you know, if you received too much subsidy you

have to pay it back.

Taxpayers who

received Forms 1095-A are encouraged to wait until March before filing their

individual tax returns. Not a problem. Surely these are people who do even meet

with their tax advisors until March.

Meanwhile,

it has finally dawned on some politicians that people may not realize the effect

of ObamaCare on them until they file their 2014 taxes. There will be rude

surprises for those who did not acquire insurance and now have to pay the

penalty. Perhaps they acquired insurance

but were over-subsidized, and now they have to repay the excess subsidy.

Wait until

they learn that the penalty will go up every year.

Then there is

a problem with the timing of obtaining health insurance. ObamaCare requires

everyone to have insurance in place by February 15 – which of course is two

months earlier than April 15, when taxes are due. That may be the first time people

understand this Rube Goldberg contraption foisted 50-shades-of-grey style upon

society. What happens then? Well, in addition to owing the penalty for 2014 it

would appear that one would also owe a penalty for some part of 2015 – at least

until one can acquire health insurance. The penalty goes month by month.

Many politicos

– not the brightest class emerging from natural selection – are now up in arms,

demanding that deadlines be changed, penalties ameliorated and so on. I suppose

there is a nuance there, but it escapes me.

Somewhat on

cue, on February 20 the Center for Medicare and Medicaid Services declaimed

that the enrollment period shall reopen from March 15 to April 30.

To which I have

two questions:

- What happened to the period from February 15 to March 15?

- Why is the Center for Medicare and Medicaid Services changing the law?

On February 13 - which seems a lifetime ago at this point - the IRS finally provided some guidance on how to comply with the new repair Regulations effective with the 2014 tax returns. Considering that their first pass at the Regulations required almost everyone with real estate or other depreciable property to file for a change in accounting method - a change which the IRS mandated, by the way - the IRS then had the temerity to say that we also had to formally ask them for permission to change. I had and have a stack of real estate partnership returns in my office waiting on their guidance. Forests have been felled by tax practitioners divining for weeks and months what the IRS wanted from us this year in order to comply with their new Regulations.

Do you ever wonder if our government is suffocating under the weight of people who - having accomplished little more than going to a name school or playing at politics - think they now have the chops to bludgeon those of us who actually accomplish something every day?

Back to our initial question though: are tax seasons getting “harder?”

I don’t think “harder” is the word I would use for for it.