Did you hear about the court

decision in Halbig, et al v Sebelius?

The suit was brought by six businesses against the employer mandate under ObamaCare.

The federal District Judge, Paul Friedman, refused a preliminary injunction against

the government, but he did say the case would be decided on an expedited

basis. That court joins Pruitt v. Sebelius,

a case from Oklahoma. There

is yet another suit to be heard by month-end in Richmond, Virginia.

What

is going on?

They are

suing over the employer penalty under ObamaCare - the $2,000 or $3,000 penalty,

depending upon whether the employer offers insurance and whether the insurance

meets politically correct criteria. The employer penalty triggers when an

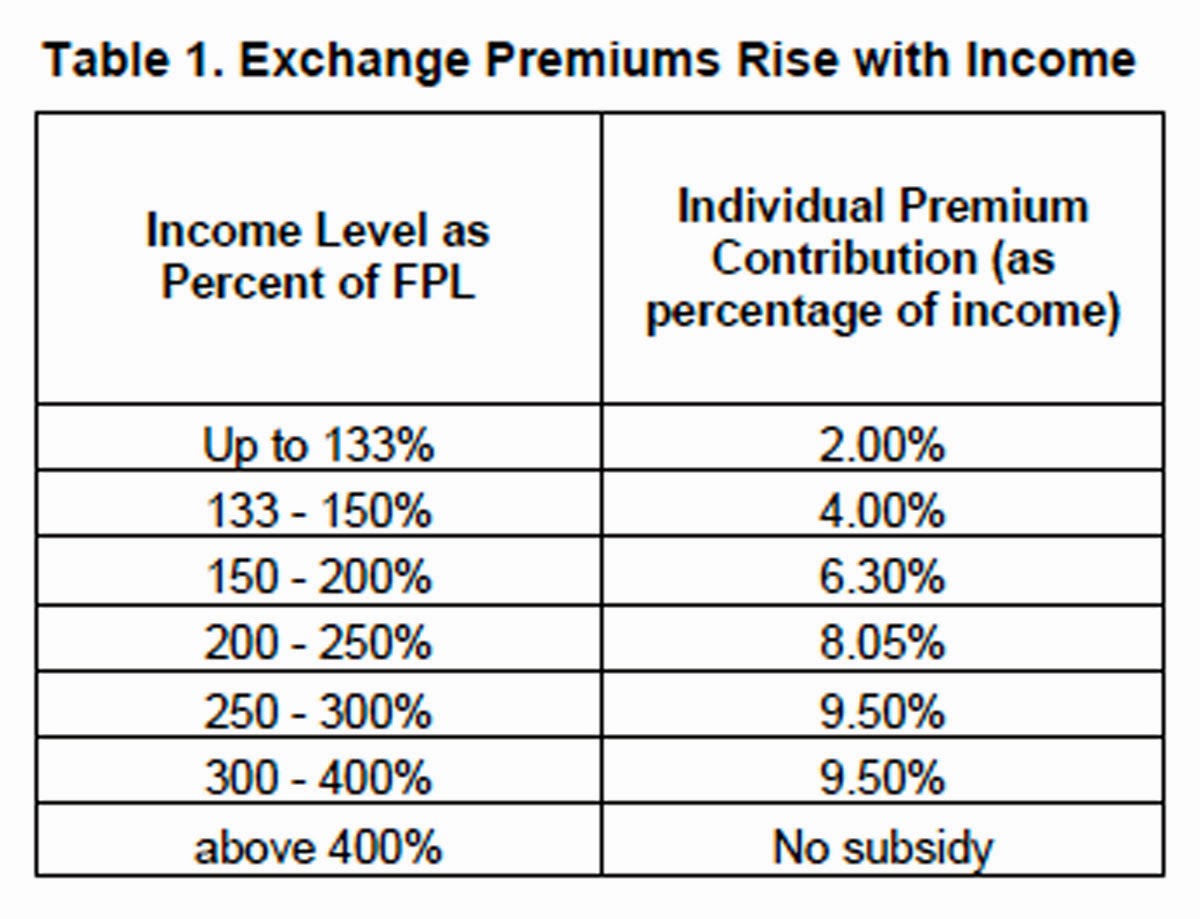

employee qualifies for a subsidy on the public exchange (the “Marketplace”).

One qualifies if one’s income is below 400% of the federal poverty line and meets

other criteria. The employer would then be required to subsidize some of the

cost through that $2,000/$3,000 penalty.

What does

it take to qualify for an individual subsidy?

Let’s do

something that Congress apparently did not do when this passed this law: let’s

read it:

Let’s

start with Section 1311(b):

Sec 1311(b) AMERICAN HEALTH

BENEFIT EXCHANGES.—

(1) IN GENERAL.—Each

State shall, not later than January 1, 2014,

establish an American Health Benefit Exchange (referred to in this title as an

‘‘Exchange’’) for the

State that…

We read

that each state is to establish an Exchange.

What if

the state fails to establish an Exchange?

Sec

1321 (c) FAILURE TO ESTABLISH EXCHANGE OR IMPLEMENT REQUIREMENTS.

(1) IN

GENERAL.—If—

(A) a State is not an electing State

under subsection (b); or

(B)

the Secretary determines, on or before January 1, 2013, that an electing State—

(i)

will not have any required Exchange operational by January 1, 2014; or

(ii)

has not taken the actions the Secretary determines necessary to implement—

(I)

the other requirements set forth in the standards under subsection (a); or

(II)

the requirements set forth in subtitles A and C and the amendments made by such

subtitles;

the Secretary shall (directly or through agreement

with a not for profit entity) establish and operate such

Exchange within the State and the Secretary shall take such actions

as are necessary to implement such other requirements.

We read that the Secretary will

establish the Exchange.

How does an individual get to a

subsidy?

SEC.

1401. REFUNDABLE TAX CREDIT PROVIDING PREMIUM ASSISTANCE FOR COVERAGE UNDER A

QUALIFIED HEALTH PLAN.

(a)

IN GENERAL.—Subpart C of part IV of subchapter A of chapter 1 of the Internal

Revenue Code of 1986 (relating to refundable credits) is amended by inserting after section 36A the following

new section:

SEC. 36B. REFUNDABLE CREDIT FOR COVERAGE

UNDER A QUALIFIED

HEALTH PLAN.

(a)

IN GENERAL.—In the case of an applicable taxpayer, there shall be allowed as a

credit against the tax imposed by this subtitle for any taxable year an amount

equal to the premium assistance credit amount of the taxpayer for the taxable

year.

(b)

PREMIUM ASSISTANCE CREDIT AMOUNT.—For purposes of this section—

(1)

IN GENERAL.—The term ‘premium assistance credit amount’ means, with respect to

any taxable year, the sum of the premium assistance amounts determined under

paragraph (2) with respect to all coverage months of the taxpayer occurring

during the taxable year.

‘‘(2)

PREMIUM ASSISTANCE AMOUNT.—The premium assistance amount determined under this

subsection with respect to any coverage month is the amount equal to the lesser

of

(A)

the

monthly premiums for such month for 1 or more qualified health plans offered in

the individual market within a State which cover the taxpayer, the taxpayer’s spouse,

or any dependent (as defined in section 152) of the taxpayer and which were

enrolled in through an Exchange established by the State under 1311

of the Patient Protection and Affordable Care Act, or

(B)

the

excess (if any) of— ‘‘(i) the adjusted monthly premium for such month for the

applicable second lowest cost silver plan with respect to the taxpayer, over

‘‘(ii) an amount equal to 1/12 of the product of the applicable percentage and

the taxpayer’s household income for the taxable year

Whoa. If the nuns taught me how

to read English, I see that the taxpayer has to be enrolled in an Exchange pursuant

to Section 1311. Section 1311 requires “each state” to do something, otherwise

Section 1321 kicks in.

Question:

What if a state does nothing (thereby removing Section 1311) and the federal

government steps in under Section 1321. Would someone in that state be receiving

a subsidy as defined under Section 1401 or not?

Can the federal government be a

“state?”

Let’s look at Section 1304(d):

Sec

1304(d) STATE.—In this title, the term ‘‘State’’ means each of the 50 States

and the District of Columbia.

Looks like the answer is “no.”

Considering that there are

approximately three dozen states that did not set-up their own Exchange, how

does the federal government propose to get an employer to pay that

$2,000/$3,000 penalty despite the language in Sections 1401 and 1311?

The IRS comes to the rescue by

proposing the following Regulation:

a taxpayer is eligible for the credit

for a taxable year if . . . the taxpayer or a member of the taxpayer’s family

(1) is enrolled in one or more qualified health plans through an Exchange established

under section 1311 or 1321 of the

Affordable Care Act . . .”

Good grief! Well, one thing about

Tony is that he could always count on Paulie and Christopher to back him up.

Does law mean nothing to this

crowd? Perhaps the law is flawed, perhaps it was poorly drafted, but it still

law. How many times have I read about unintended consequences of the

alternative minimum tax or about some poor taxpayer being hung out to dry because

he/she did not get that “special” piece of paper the IRS wanted in order to substantiate

a transaction? How did the IRS invariably

defend its position? By arguing that the law is the law and that Congress

should remedy any inequity.

In a swell of self-importance, the Administration and its

enablers refuse to accept that the same law that applies to you or me also applies to them. Instead they argue that:

(1) Justice Roberts

decided that the penalties are a tax. The Anti-Injunction Act precludes

plaintiffs from challenging the imposition of a tax before it is actually

assessed.

(2) The plaintiffs

lack standing due to the speculative nature of any claimed injuries.

(3) Following the

White House announcement of the one-year delay of the employer mandate, the court

should also delay its consideration.

(4) The language

around subsidies represents but one of the ACA’s many drafting errors.

(5) Congress clearly

intended to have tax credits available in all the states.

Let me get

this straight: their argument is that Tony did not clearly intend for me to defend

myself until after I was shot, because before then any self-defense would be

speculative and contingent on the actions of someone for whom English is a

second language.

Really?

Really?

Let us

review history to understand how we got into this mess. The House had a bill.

The Senate had a bill. The bills were different. The Senate wanted to force the

states to absorb the Exchanges, but it ran into a problem with Pritz v United States (1997):

[T]he

Federal Government may not compel the states to implement, by legislation or

executive action, federal regulatory programs.’’

The Senate

instead added a provision for federally established exchanges as a backup

option for states that refused to set up exchanges.

Remember

that bill could not obtain bipartisan support, and it was passed on a Saturday

night at late hour, after the Louisiana Purchase, the Cornhusker Kickback and

who-knows-what-else. The Democrats had lost their Senate 60-vote majority in

January 2010, meaning they could not override the expected filibuster. To push the bill through the Senate, Reid forced

a reconciliation vote - a tactic normally reserved to limit debate on budget

bills. This tactic however did not allow for a normal Senate-House joint

committee process to reconcile burrs in the law. How could it? It was designed for

budget and debt ceiling items, not for something like this.

Let’s see what happens in Halbig and Pruitt. Judge Paul Friedman hopes to have his opinion out by

February.